Abstract

Die Neugewichtung eines Portfolios ist der Prozess, alle Assetklassen eines Portfolios hinsichtlich ihrer Gewichtung wieder wie gewünscht auszurichten. Sie bringen Ihr Portfolio wieder zur gewünschten Mischung von Aktien, Bonds, Cash und anderen Produkten zurück, wenn sie nicht mehr mit Ihren Plänen oder Limiten übereinstimmen.

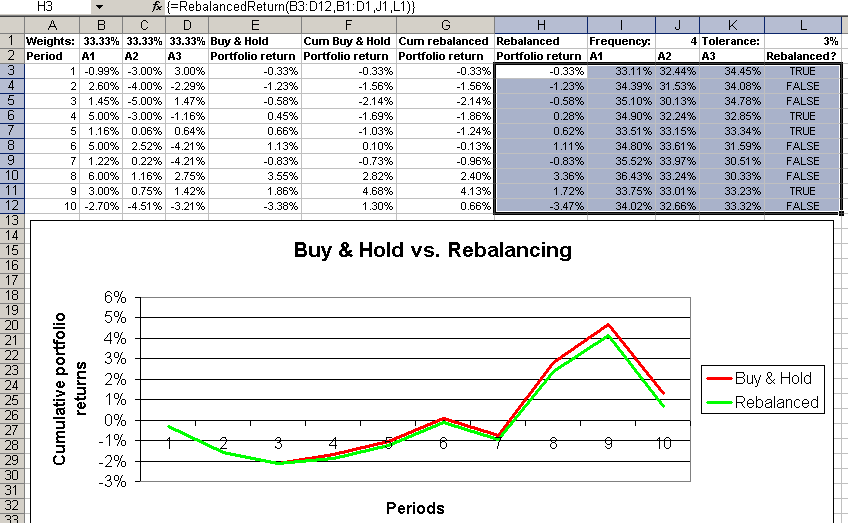

Ein Beispiel:

Appendix – Programmcode sbRebalancedReturn

Bitte den Haftungsausschluss im Impressum beachten.

Option Explicit

Const CMaxDouble = 1.79769313486231E+308

Function sbRebalancedReturn(rARM As Range, _

rIWV As Range, _

Optional ByVal lRF As Long = 0, _

Optional dDT As Double = CMaxDouble) As Variant

'RebalancedReturn calculates balanced returns for a

'portfolio with given

'rARM - asset return matrix (columns show different

' assets, rows show returns per asset over time)

'rIWV - initial weight vector for the assets

'lRF - rebalancing frequency (in time steps = rows)

' If lRF > 0 then each lRF time step rebalancing

' will take place

' If lRF = 0 then no rebalancing will take place

' If lRF < 0 then each -lRF time step after last

' rebalance portfolio will be rebalanced again

'dDT - drift tolerance %, if any asset has drifted by

' by more than dDT (relative measure) then the

' portfolio will be rebalanced AND the internal

' rebalancing frequency count will be reset

'The output matrix shows portfolio returns % in first

'column, then end-of-period asset weights and finally

'boolean output values in last column, showing whether

'a rebalance happened.

'This function has been inspired by Andreas Steiner's

'similar function.

'Source (EN): http://www.sulprobil.de/sbrebalancedreturn_en/

'Source (DE): http://www.berndplumhoff.de/sbrebalancedreturn_de/

'(C) (P) by Bernd Plumhoff 19-Mar-2011 PB V0.2

Dim i As Long, j As Long, k As Long, n As Long, m As Long

Dim bDrifted As Boolean, bForceRB As Boolean

n = rARM.Rows.Count 'Number of observations

m = rARM.Columns.Count 'Number of assets

If m <> rIWV.Columns.Count Or _

rIWV.Rows.Count <> 1 Then

sbRebalancedReturn = CVErr(xlErrValue)

Exit Function

End If

ReDim w0(1 To m) As Double, x(1 To m) As Double

ReDim r(1 To n, 1 To m) As Double

If lRF = 0 Then lRF = n

If lRF < 0 Then

lRF = -lRF

bForceRB = True

Else

bForceRB = False

End If

ReDim vR(1 To n, 1 To m + 2)

For i = 1 To m

x(i) = rIWV(i)

w0(i) = x(i)

For j = 1 To n

r(j, i) = rARM(j, i)

Next j

Next i

k = 1

'Model rebalancing tolerance

For i = 1 To n

If bDrifted And bForceRB Then k = i

'Calculate period start weights

vR(i, m + 2) = (i - k) Mod lRF = 0 Or bDrifted

If vR(i, m + 2) Then

For j = 1 To m

x(j) = w0(j)

Next j

Else

For j = 1 To m

x(j) = vR(i - 1, 1 + j)

Next j

End If

'Calculate portfolio return

For j = 1 To m

vR(i, 1) = vR(i, 1) + x(j) * r(i, j)

Next j

'Calculate period end weights & check for drift

bDrifted = False

For j = 1 To m

vR(i, 1 + j) = x(j) * (1# + r(i, j)) / (1# + vR(i, 1))

bDrifted = bDrifted Or Abs(vR(i, 1 + j) - w0(j)) > dDT

Next j

Next i

sbRebalancedReturn = vR

End Function

Download

Bitte den Haftungsausschluss im Impressum beachten.

sbRebalancedReturn.xlsm [25 KB Excel Datei, ohne jegliche Gewährleistung]